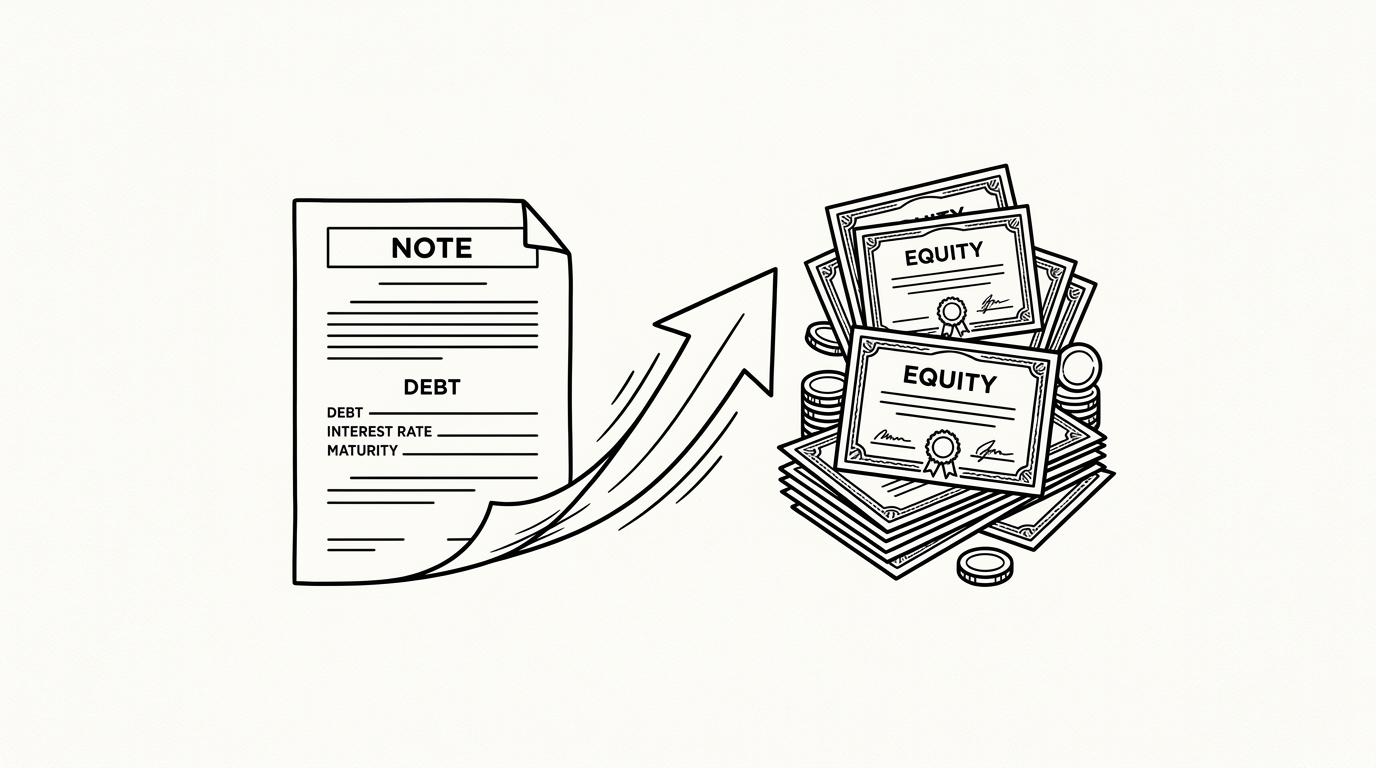

Convertible Note

Convertible note is a form of startup financing structured as debt that is intended to convert into equity at a future priced financing round; An investor loans money to the startup under the convertible note agreement; Convertible notes are still used in certain contexts: when investors prefer the debt structure for legal or tax reasons, in jurisdictions where SAFEs are not well established, or for bridge rounds between priced rounds where the note structure can be cleaner

Convertible note is a form of startup financing structured as debt that is intended to convert into equity at a future priced financing round. It bears an interest rate (typically 4-8% annually) and has a maturity date (usually 18-24 months) by which it must either convert to equity or be repaid. Like a SAFE, it often includes a valuation cap and/or a discount rate that give early investors a more favorable conversion price than later investors. Convertible notes were the dominant early-stage instrument before SAFEs became widespread.

How it works

An investor loans money to the startup under the convertible note agreement. Interest accrues on the principal amount (typically it is accrued, not paid in cash, and added to the conversion amount). At a qualifying financing event (a priced equity round above a certain size threshold), the principal plus accrued interest converts to equity at the better of the cap price or the discounted price. If the company reaches the maturity date without triggering a conversion event, the noteholders can demand repayment or negotiate a conversion at the current valuation.

Key facts

- Key difference from SAFE: Convertible notes are debt with interest and a maturity date; SAFEs are not debt and have neither, making SAFEs simpler and lower-risk for founders.

- Conversion discount: A typical 20% discount means noteholders convert at 80% of the Series A price, rewarding their early-stage risk.

- Maturity risk: If a priced round never happens before maturity, noteholders may have leverage to demand repayment or unfavorable conversion terms.

For builders

Convertible notes are still used in certain contexts: when investors prefer the debt structure for legal or tax reasons, in jurisdictions where SAFEs are not well established, or for bridge rounds between priced rounds where the note structure can be cleaner. For most first-time founders raising an initial seed from US angels, the SAFE has superseded the convertible note due to its simplicity and lack of debt mechanics. The maturity date risk is the most important factor: raising a convertible note and not closing a priced round before maturity can create significant leverage for noteholders at a vulnerable moment.

Sources

- Y Combinator. SAFE (Simple Agreement for Future Equity) standard documents. ycombinator.com

- U.S. SEC. Exempt offerings and small-business capital raising. sec.gov

- National Venture Capital Association. Model legal documents. nvca.org

- Kauffman Foundation. Startup research and entrepreneurship data. kauffman.org

- Federal Reserve. Small Business Credit Survey. federalreserve.gov